Microsoft's Xandr DSP closure opens doors for independent players

Adform CTO sees €100 billion European opportunity as privacy concerns drive market consolidation.

Microsoft's decision to shutter its demand-side platform (DSP) has created a significant opening for independent ad tech companies, according to Jochen Schlosser, Chief Technology Officer at Adform. The announcement, made on May 14, 2025, marked the end of Microsoft Invest, formerly known as Xandr and originally AppNexus, effective February 28, 2026.

In a detailed discussion on ExchangeWire's Trader Talk TV on May 23, Schlosser addressed the broader implications of this closure for the programmatic advertising landscape. According to Microsoft Advertising Corporate Vice President Kya Sainsbury-Carter, the company is "exclusively focusing our buy-side advertising technology investments on the Microsoft Advertising Platform" starting in 2026, pivoting toward what they describe as AI-driven, conversational advertising solutions.

Get the PPC Land newsletter ✉️ for more like this.

Summary

Who: Jochen Schlosser, Chief Technology Officer at Adform, discussed the implications of Microsoft's decision to close its Xandr DSP platform during an ExchangeWire interview.

What: Microsoft announced the closure of Microsoft Invest (formerly Xandr/AppNexus DSP) effective February 28, 2026, citing a strategic pivot toward AI-driven advertising solutions and privacy concerns.

When: The announcement was made on May 14, 2025, with Schlosser's analysis following on May 23, 2025.

Where: The closure affects global programmatic advertising markets, with particular impact on European independent DSP operations where competition has become increasingly concentrated.

Why: Microsoft cited the need to focus on "conversational, personalized, and agentic" advertising futures incompatible with traditional DSP models, though Schlosser questioned the privacy rationale and sees the move creating opportunities for independent players in the expanding open web market.

The closure represents more than just a corporate restructuring. Microsoft cited privacy concerns as a primary driver, but Schlosser questioned this rationale. "The only thing that can happen is that you take this one out and you're adding Trade Desk or you're adding Adform," he explained during the broadcast. "So you're actually adding a third party DSP removing your own DSP because this is an end-to-end platform privacy. So there's one vendor that needs consent. Here there are two vendors. So out of the box I don't really see if you are an end-to-end platform which is bridging the entire supply chain in a privacy compliant matter."

His analysis suggests that Microsoft's end-to-end approach was actually more privacy-compliant than requiring third-party DSP integrations, contradicting the stated reasoning for the closure.

The programmatic advertising market has experienced substantial growth despite challenges. According to IAB Europe's AdEx Benchmark Report released on May 21, 2025, European digital advertising reached €118.9 billion with 16% year-over-year growth in 2024. Programmatic advertising demonstrated renewed vitality with 18.4% expansion, reaching €15.5 billion across Europe, marking a recovery from slower growth in 2023.

Get the PPC Land newsletter ✉️ for more like this.

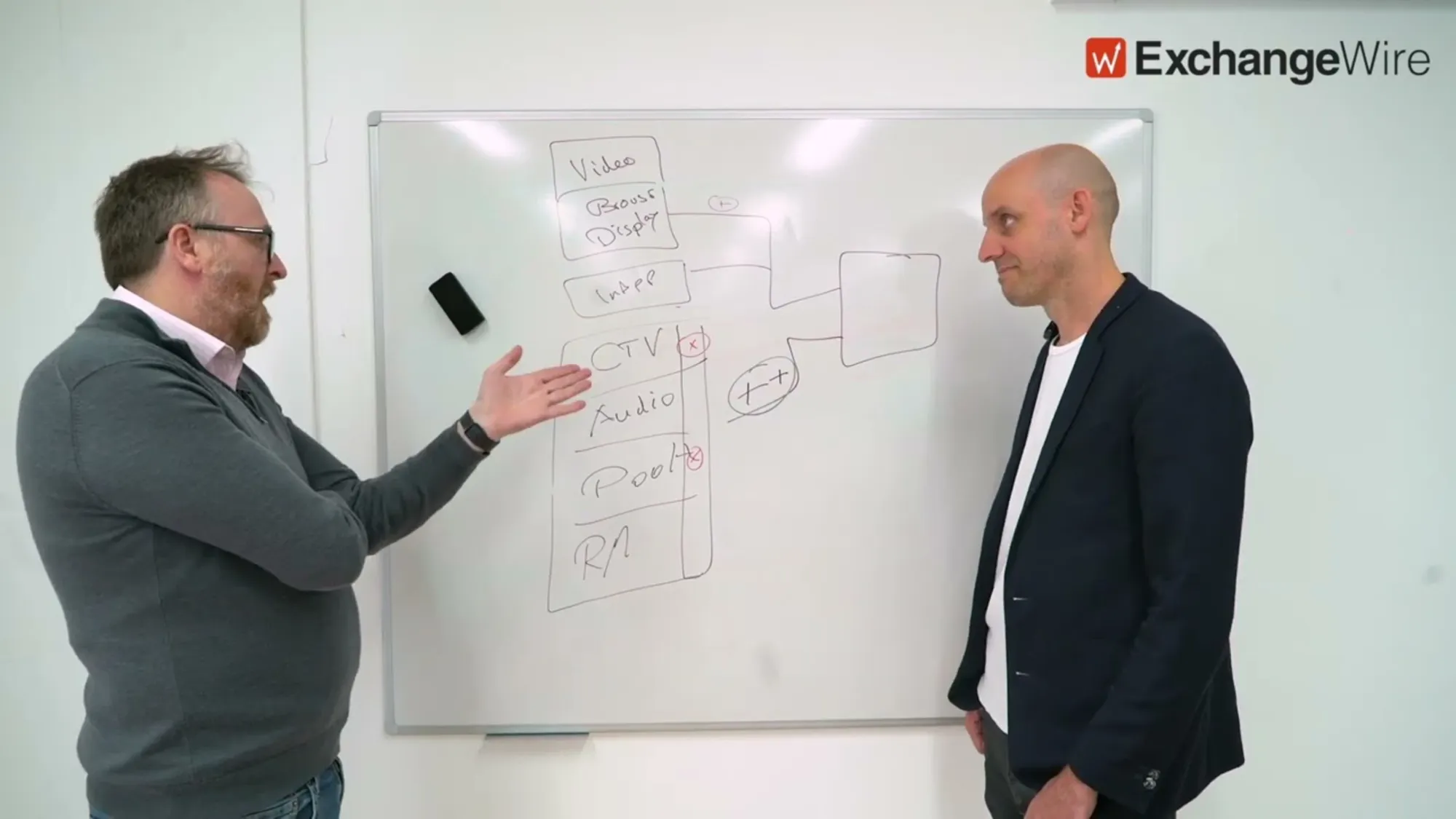

Schlosser sees enormous opportunity in what he terms the "open web," which extends far beyond traditional browser-based display advertising. He outlined a market size of approximately €100 billion in Europe alone, encompassing connected television (CTV), audio, digital out-of-home advertising, and retail media networks.

"When we are talking with our strategists also with external consultants we are more and more focusing not just on the display piece of course same protocol same browser but an increasing part of video more and more and more every year of course also video as a main format going into CTV then we have audio rising quite massively and we have digital out of home really coming out of the box," Schlosser explained.

The breakdown reveals shifting market dynamics. According to Schlosser's analysis, traditional browser-based display advertising represents roughly 70% of current programmatic spending, while emerging channels account for approximately 30%. However, these proportions are evolving rapidly, with video, CTV, and audio formats driving significant growth.

Connected television particularly stands out as a growth driver. The format benefits from major streaming platforms expanding their advertising capabilities across European markets. Meanwhile, large technology companies like Google, Meta, and Amazon increasingly focus on their own inventory rather than open web opportunities, creating space for independent DSPs.

"Who are the big CTV players? That's the big streaming platform," Schlosser noted. "They're not really playing here because effectively they're just basically buying their own stuff."

The artificial intelligence component of Microsoft's strategy announcement also drew scrutiny. Schlosser emphasized that existing ad tech infrastructure already incorporates extensive AI capabilities. "The classic Adform, the one that existed already 2019, is built on top of an AI stack right and that is around 20 AI services transactional always on more than 40,000 bidding models deployed a couple of times a day," he detailed.

Get the PPC Land newsletter ✉️ for more like this.

Rather than replacing existing systems, Schlosser envisions agentic AI as an additional user interface layer. The technology will enable more intuitive interaction with complex programmatic systems without fundamentally altering underlying optimization engines. "You will add a new UI layer and that is an agentic AI layer," he explained, comparing it to conversational interfaces that simplify complex tasks without changing backend functionality.

This perspective challenges the narrative that AI represents a complete transformation of ad tech infrastructure. Instead, it suggests evolutionary improvement through enhanced user experience and navigation capabilities.

The departure of Microsoft from independent DSP operations leaves fewer major players in the European market. Schlosser noted that "there's only two left at this stage if Google at least in Europe," highlighting the concentration of demand-side platforms.

Industry data supports continued programmatic growth despite consolidation concerns. According to Comscore's State of Programmatic Report released on January 21, 2025, 72% of marketers plan to increase their programmatic advertising investment in 2025, marking a significant rise from 62% in 2024.

The evolution toward privacy-first advertising approaches also creates opportunities for independent players. Connected TV emerges as a dominant force, with its share of media budgets projected to double from 14% in 2023 to 28% in 2025, while traditional targeting methods face limitations.

Audio and digital out-of-home advertising represent additional growth channels largely outside the control of major walled gardens. Retail media networks continue expanding, with every major retailer launching advertising businesses. These developments create diverse inventory sources that require aggregation through independent DSPs.

The complexity of managing multiple channels and inventory sources reinforces the value proposition for independent platforms. "Does the agency want to operate the four gardens with a specific system? Then the five biggest CTV publishers then a couple of digital home players that all have their own buyer interface?" Schlosser questioned, highlighting the operational challenges of fragmented direct relationships.

Supply path optimization initiatives have enhanced programmatic advertising quality by reducing intermediary layers and improving transparency. First-party data integration has partially compensated for third-party cookie limitations, enabling more sophisticated audience targeting strategies.

The technical infrastructure supporting programmatic advertising continues evolving. Machine learning improvements focus on driving incremental performance across campaign types, while frequency management solutions address cross-platform optimization challenges.

Microsoft's pivot toward AI-driven advertising solutions may signal broader industry trends, but independent DSPs maintain advantages in transparency, control, and cross-channel capabilities. The open web opportunity spans multiple formats and inventory sources that require sophisticated aggregation and optimization.

Market concentration among demand-side platforms could accelerate following Microsoft's exit. However, the growing diversity of inventory sources and advertising formats creates ongoing demand for independent technology solutions capable of managing complex programmatic ecosystems.

The European market's strong growth trajectory, combined with expanding inventory sources beyond traditional display advertising, positions independent DSPs for continued expansion despite competitive pressures from major technology platforms focused on owned-and-operated inventory strategies.

Get the PPC Land newsletter ✉️ for more like this.

Timeline

- May 14, 2025: Microsoft announces Xandr DSP closure effective February 28, 2026

- May 21, 2025: IAB Europe releases AdEx report showing €118.9 billion European digital advertising market

- May 23, 2025: Adform CTO Jochen Schlosser discusses implications on ExchangeWire Trader Talk TV

- January 21, 2025: Comscore releases State of Programmatic Report showing 72% growth in investment plans

- June 16, 2025: Netflix adds Yahoo DSP as fourth global programmatic partner

- June 10, 2025: Comscore expands certified deals with Adelaide attention metrics

- December 7, 2024: X platform expands programmatic access with competitive $0.39 CPMs